“Adopt the pace of nature: her secret is patience.”

~ Ralph Waldo Emerson

- Geopolitical risk has re-entered the market narrative, keeping day-to-day sentiment fragile.

- Energy prices have moved higher, reviving near-term inflation concerns.

- Volatility has picked up as investors reprice growth, inflation, and policy paths in real time.

- History suggests disciplined, diversified, long-term positioning tends to be rewarded through drawdowns.

Spring has a way of resetting perspectives. Days get longer, routines shift, and attention naturally moves from what just happened to what comes next. That transition can feel refreshing but it can also be a reminder that change is constant, whether in the seasons or in markets.

Against that backdrop, recent market moves have felt noisy and fast-moving. Before diving into the details, it’s worth taking a step back and placing today’s headlines in a longer-term context. Markets are navigating a familiar mix: geopolitical uncertainty, higher energy prices, and renewed debate about inflation and monetary policy. When these forces collide, day-to-day price moves can feel amplified because investors are weighing several moving parts at once—growth, inflation, interest rates, and risk appetite.

Our approach in this environment is to stay process-driven: keep portfolios aligned to long-term objectives, maintain diversification across equity, rates, and credit exposures (amongst many others), and use volatility as an opportunity to rebalance rather than react. The goal is not to anticipate the next headline. Having the pieces in place to follow a plan designed for a range of market environments will help prepare for the next headlines.

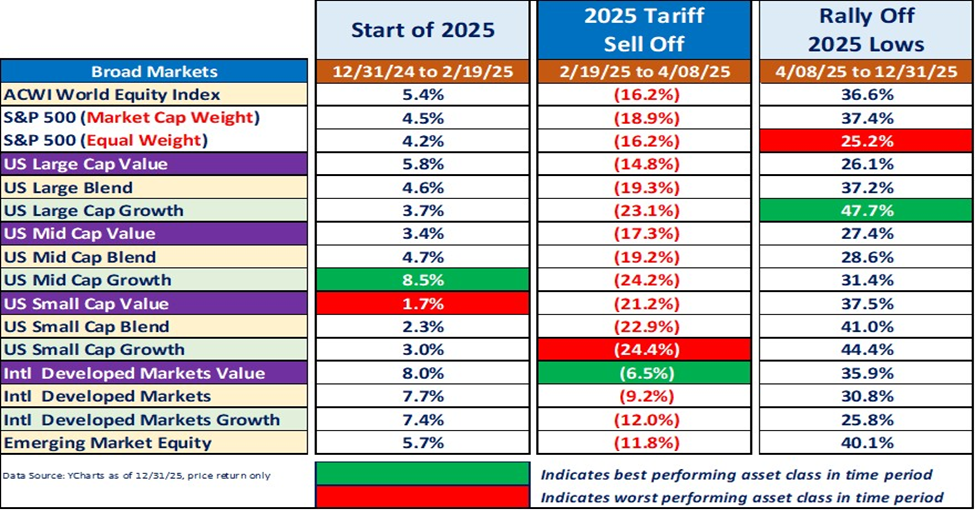

Instead of making portfolio changes based on short-term market swings, long-term investors are watching how energy prices, inflation expectations, and policy communication evolve, along with broader measures such as market breadth, credit spreads, and funding conditions. Investors are also reminded of last April, when the so-called “liberation day” sent markets reeling based on the uncertainty surrounding tariff policy. The graph below shows the rapidity of the market movements and various asset class price swings, and with hindsight, the opportunity created.

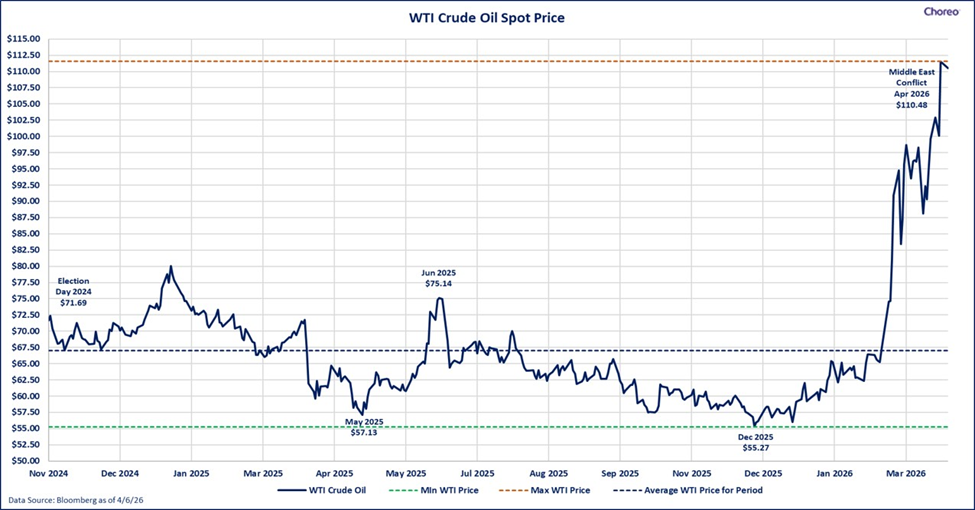

Currently, oil prices are serving as the primary source of volatility. The ongoing war in the middle east, and constraints moving oil through the Strait of Hormuz, which normally sees roughly 20% of the world’s oil supply flow, has created supply constraints for the commodity, and wild price fluctuations. Following talks, a short-term ceasefire sent prices lower, but much remains to be worked out.

It can help to separate headlines from signals. In periods like this, markets broadly tend to reprice (1) inflation risk (in this case with a rise in energy prices), (2) the level and timing of interest rates, and (3) the range of growth outcomes. That often shows up as higher volatility, wider performance dispersion across sectors, and faster rotations in leadership.

In fixed income, the market often balances two concerns that can appear at the same time: slowing growth and stubborn inflation. When energy is a key driver, investors may worry about consumer purchasing power (a growth headwind) while also reassessing the inflation path (a rate headwind). The practical implication is that rate expectations can shift quickly.

Credit markets can be a useful “stress gauge.” When uncertainty rises, investors watch whether spreads1 widen materially, refinancing becomes more difficult, or liquidity deteriorates. A moderate repricing can be typical in risk-off periods; more persistent widening and weaker market liquidity would be more meaningful signs of tightening financial conditions.

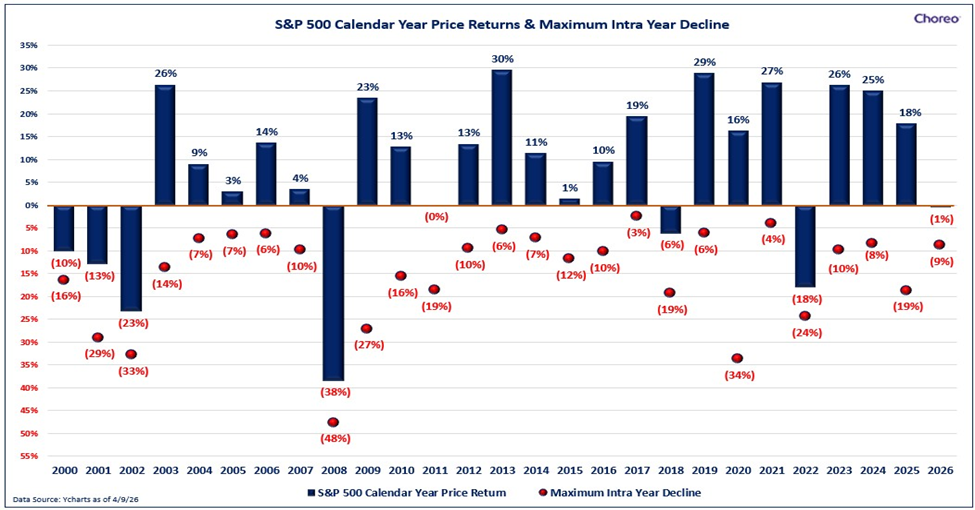

Equities often reprice in two steps: first through valuations (due to changes in investor sentiment and discount rates), and later through earnings (fundamentals). Volatile periods can compress valuations2 quickly, then stabilize as investors gain clarity on whether fundamentals are changing. The graph below shows the annual S&P performance with the blue bar representing the year’s performance, while the red dot demonstrates the intra-year decline.

1Spread is the difference between the yield on a corporate bond and a comparable maturity Treasury. It reflects the additional yield investors demand for taking on additional risk.

2As measured by common financial ratios such as price/earnings. In this case, price coming down while earnings remain unchanged would result in a lower, and thus compressed, valuation.

An evolving global backdrop

Geopolitical tensions in the Middle East have added uncertainty, and markets are evaluating potential spillovers beyond the region. Because energy markets sit at the intersection of geopolitics and inflation, heightened tensions can contribute to higher and more volatile oil and gasoline prices. When that happens, investors often re-examine assumptions about the inflation path. Higher energy costs can filter into transportation, logistics, and everyday goods—an example of how external shocks can change the economic discussion quickly, although the real-world ramifications depend on how long the shock lasts, typically requiring the underlying commodity to sit at higher prices for an extended period of time.

Inflation, rates, and the policy reaction function

Energy-driven inflation is different from demand-driven inflation. It can act like a tax on households and businesses, weighing on consumption, while also lifting headline inflation readings. That combination is one reason markets can feel unsettled even if broader economic data has not materially changed.

A practical question is whether higher energy prices remain a one-time level shift or begin to influence broader pricing behavior. We watch for potential “second-round” effects—services inflation, wage dynamics, and longer-term inflation expectations because those inputs can shape how markets interpret inflation risk.

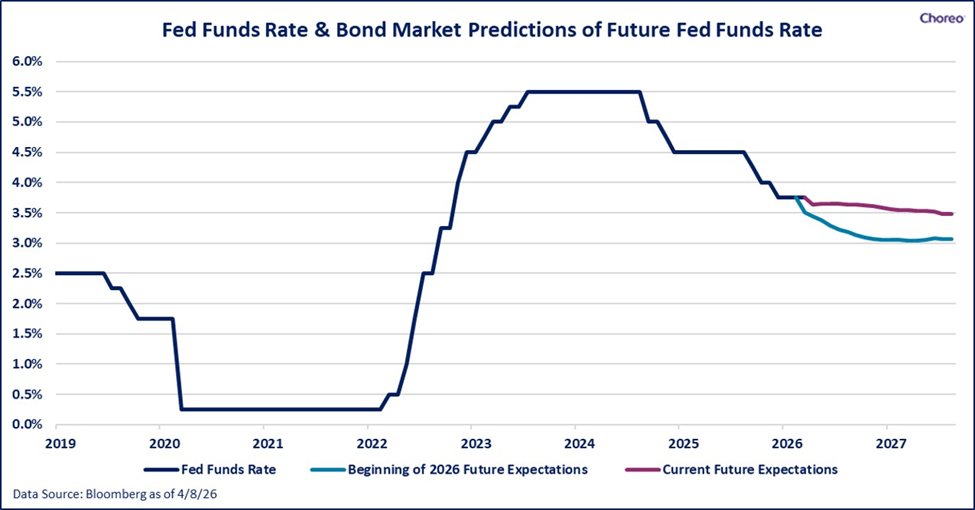

Central banks generally aim to balance two risks: easing too soon and allowing inflation pressures to re-emerge or staying too restrictive and slowing growth more than intended. Incoming inflation data, inflation expectations, and overall financial conditions can influence how policymakers communicate and how markets price the path of rates. Case in point, all the current news flow has led markets to effectively re-price expectations from two interest rate cuts this year to zero as shown in the graph below.

One year later: a reminder about recoveries

Markets are also nearing the one-year mark since “Liberation Day,” a period that included a sharp equity drawdown followed by an equally impressive rebound. While every episode is different, the broader reminder is consistent: periods of stress can arrive quickly, and turning points are often hard to time.

Historically, drawdowns tied to geopolitics, economics, or policy have been followed by recoveries over time, although the timing and magnitude can vary widely. The key takeaway is simple: markets rarely move in a straight line. Volatility is uncomfortable, but it is also a normal feature of long-term investing.

Equities: fundamentals versus headlines

Equity selloffs can feel like a verdict on the economy, but they are often a rapid repricing of discount rates and risk premiums. Over longer horizons, equity results tend to be driven primarily by earnings growth and cash flows. Higher energy prices and a higher rate backdrop can affect sectors differently. Some areas may benefit from stronger commodity pricing, while more rate-sensitive segments can face valuation pressure. Dispersion like this is one reason diversification across sectors and styles can matter more than usual in volatile regimes.

Volatility is the price of admission

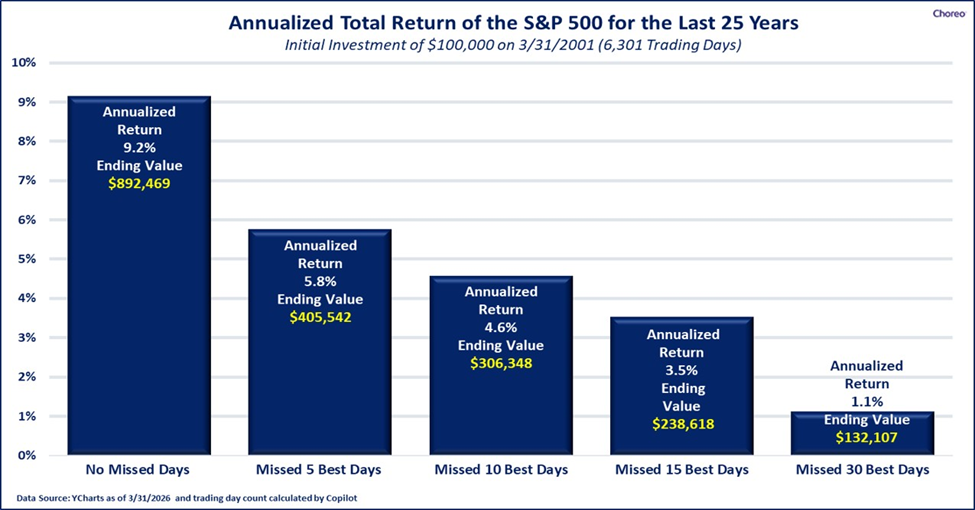

The mix of geopolitical uncertainty and shifting inflation expectations has lifted volatility. That is not a sign markets are “broken”—it reflects markets that are continuously updating prices as new information arrives.In these moments, headlines can tempt investors into short-term moves. A recurring challenge is that large up days often cluster near large down days, which can make exit-and-reentry decisions difficult in real time. It is virtually impossible to time markets effectively. Discipline is the critical factor, removing emotion and focusing on the plan. The graph below demonstrates that the winning factor is normally patience.

Looking Ahead

Looking ahead, investors will continue to weigh how geopolitics, energy prices, inflation trends, and policy communication interact and how those factors affect risk sentiment. In the near term, markets may remain sensitive to incremental information and shifts in expectations. That uncertainty is one reason a long-term plan, diversification, and a repeatable decision framework can be valuable. For long-term investors, the more actionable focus is on maintaining an allocation designed for a range of outcomes and using a rebalancing discipline to manage risk through market swings.

Conclusion

Volatility is not a detour from investing—it’s part of the journey. Geopolitical events and inflation scares can create short-term dislocation, but markets have historically adjusted over time. The objective is less about predicting what happens next and more about staying diversified and aligned to a long-term plan through changing conditions. The objective is to keep risk aligned with goals, so short-term volatility does not force long-term decisions. As always, we encourage you to reach out to your Choreo advisor with additional questions.

Important Disclosures

Opinions are as of the date referenced and are based on sources considered reasonable by Choreo. Opinions are subject to change based on market or economic conditions. There is no guarantee that any of these expectations will become actual results.

The performance numbers displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Past performance does not indicate future performance. The indices discussed are unmanaged and do not incur management fees, transaction costs or other expenses associated with investable products. It is not possible to directly invest in an index.

This document contains general information, may be based on authorities that are subject to change, and is not a substitute for professional advice or services. This document does not constitute audit, tax, consulting, business, financial, investment, insurance, legal or other professional advice, and you should consult a qualified professional advisor before taking any action based on the information herein. Information has been obtained from a variety of sources believed to be reliable though not independently verified. Choreo, LLC, its affiliates and related entities are not responsible for any loss resulting from or relating to reliance on this document by any person. Internal Revenue Service rules require us to inform you that this communication may be deemed a solicitation to provide tax services. This communication is being sent to individuals who have subscribed to receive it or who we believe would have an interest in the topics discussed. Past performance does not indicate future performance. The sole purpose of this document is to inform, and it is not intended to be an offer or solicitation to purchase or sell any security, or investment or service. Investments mentioned in this document may not be suitable for investors. Before making any investment, each investor should carefully consider the risks associated with the investment and make a determination based on the investor’s own particular circumstances, that the investment is consistent with the investor’s investment objectives.

All registered trademarks are intellectual property of Choreo, LLC. © 2026 Choreo, LLC. All Rights Reserved.