“The essence of investment management is the management of risks, not the management of returns.”

~ Benjamin Graham

- The Federal Reserve (the “Fed”) remains at the center of the market narrative, balancing its dual mandate of price stability and maximum employment as inflation continues to ease, but not yet enough to declare victory.

- Economic data remain generally supportive, with steady growth and resilient labor markets limiting the urgency for aggressive rate cuts, even as market expectations fluctuate.

- Leadership at the Fed is coming into sharper focus, with the nomination of a new Chair adding another layer of uncertainty and underscoring why communication and credibility matter as much as policy itself.

The Middle East has once again become a tinder box of activity, and markets have become volatile. The obvious reason for many may be the event itself. For economists and market watchers, the events which have unfolded over the last several weeks have deeper contextual complications. For most people, the economy doesn’t show up as a simple chart or a headline, it shows up in everyday decisions. It’s the interest rate on a mortgage or car loan, the cost of groceries, or the question of whether it makes sense to refinance, invest, or simply wait. Behind many of those decisions sits the Federal Reserve, quietly influencing financial conditions through interest rates and policy choices that affect households and businesses alike. Understanding what the Fed does, and why it does it, can provide a clearer perspective on recent market headlines. Right now, with oil price volatility spiking due to the Middle East conflict, inflationary pressures will mount. At the same time, the employment picture is cloudy. The Fed is the body that confronts these issues and, with it, sets policy.

What Does the Federal Reserve Do?

At its core, the Federal Reserve exists to help keep the U.S. economy on stable footing. While the institution can seem opaque at times, its mission is quite straightforward. The Fed is charged with a dual mandate:

- Promote maximum employment, and

- Maintain price stability, commonly defined as stable inflation, averaging around 2% over time.

To pursue these goals, the Fed primarily adjusts short‑term interest rates and manages liquidity within the financial system. Lower rates are intended to stimulate borrowing and economic activity; higher rates are used to cool demand and lower inflation. Higher rates create an environment where purchasing homes with mortgages and buying cars with loans is more expensive, creating a larger burden for consumers. This can reduce a household’s available cash and thereby cool demand. Importantly, these tools work with long and variable lags, meaning the effects of today’s decisions often show up months, or even years, later.

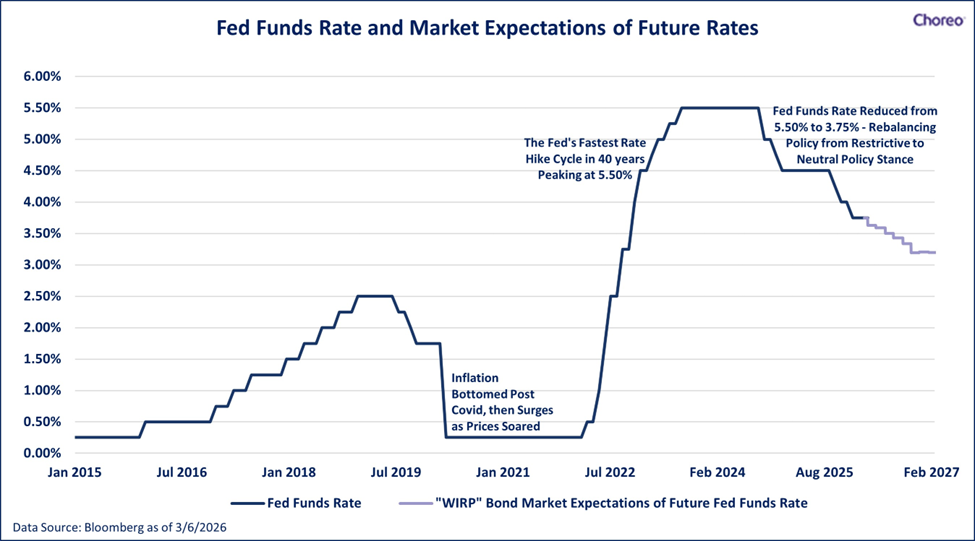

This is why Fed policy is as much about judgment and communication as it is about data. Markets don’t just react to what the Fed does — they react to what the Fed signals it might do next. Often by the time an interest rate move occurs, it is entirely anticipated by markets. The chart below illustrates the historical fed funds rate, as well as the future path of rates expected by markets as of March 6th.

The Current Economic Backdrop

As we move through early 2026, the economy remains on reasonably solid footing. Growth has held up better than many feared, supported by steady consumer spending and resilient labor markets. Unemployment remains low by historical standards, and while job growth has moderated, there is little evidence of a sharp deterioration.

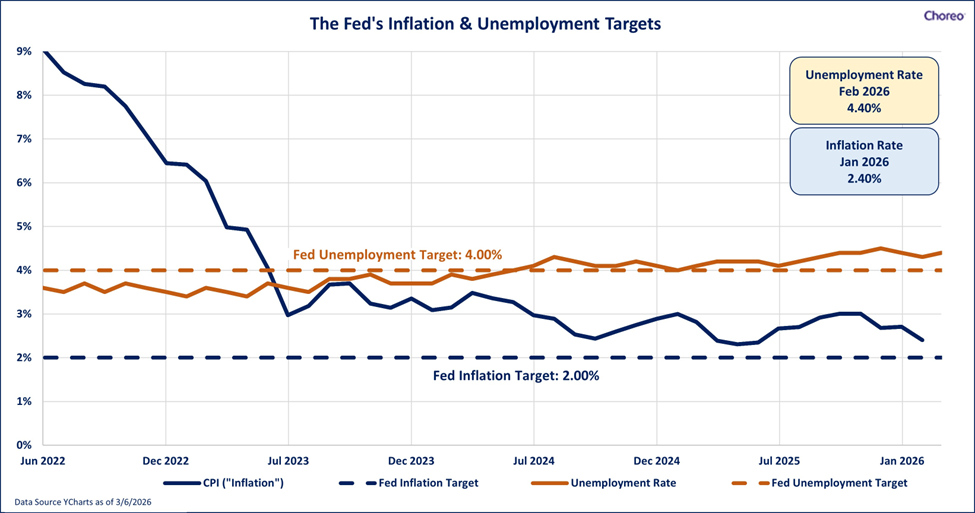

Inflation, however, continues to complicate the picture. While price pressures have eased meaningfully from their peaks, inflation remains above the Fed’s 2% target. This has made policymakers cautious, even as markets periodically anticipate a faster pace of rate cuts. The result is a familiar push and pull: investors hoping for easier monetary policy (via lower rates), while the central bank is focused on not declaring victory too soon (i.e. lowering rates). The chart below shows the current state of the dual mandate.

Monetary Policy: Between Patience and Pressure

The Fed’s current stance reflects this tension. Stronger economic data limits the urgency to cut rates aggressively, while political and market pressure argues for some degree of relief. As it stands, the Fed may have only modest scope to lower rates over the coming year, potentially limited to one or two quarter‑point rate cuts. The current data of course could change rapidly, although the trend will likely need to be longer than a handful of data points to cause more aggressive moves. This is not a backdrop for dramatic policy shifts. Instead, it is one that favors incremental moves, careful messaging, and an emphasis on credibility which brings leadership into sharper focus.

Why Fed Leadership Matters

While monetary policy decisions are made by committee, the Chair of the Federal Reserve plays a central role in shaping how those decisions are framed, communicated, and ultimately interpreted by markets. At times like this, when inflation is still above target and expectations are finely balanced, credibility and consistency matter. This is why the nomination of Kevin Warsh as the next Fed Chair (to replace Chair Jerome Powell) has attracted significant attention.

Warsh brings a blend of policy experience, market knowledge, and academic engagement. He earned a bachelor’s degree in public policy from Stanford University and a law degree from Harvard Law School. His early career included work in mergers and acquisitions at Morgan Stanley before transitioning into public service.

In 2006, Warsh was appointed to the Federal Reserve Board of Governors, becoming the youngest person ever to serve on the Board. During the Global Financial Crisis, he played a role in policy discussions and represented the Fed in international forums, including the G‑20. He served on the Board until 2011.

Following his time at the Fed, Warsh remained active in both finance and academia, including roles at a family office and as a fellow and lecturer at Stanford. He was previously a finalist for Fed Chair prior to Jerome Powell’s appointment in 2017 and was formally nominated for the role on January 30, 2026.

The Confirmation Process and Why Markets Care

The path forward follows a familiar process. After presidential nomination, the Senate Banking Committee reviews the nominee’s background and holds confirmation hearings focused on monetary policy, inflation, regulation, and economic outlook. A committee vote is followed by a full Senate vote, with confirmation requiring a simple majority. The timing of the confirmation can be summarized and loosely scheduled to occur over the following key dates:

| Event Date | Nomination Process Activity |

| March 4, 2026 | White House submits Kevin Warsh nominations to the U.S. Senate (Fed Governor& Fed Chair) |

| Mid-March 2026 | Nomination referred to the Senate Banking, Housing, and Urban Affairs Committee |

| Mid- to Late- March 2026 | Senate Banking Committee confirmation hearing |

| April 2026 | Senate Banking Committee vote to advance the nomination to the full Senate |

| April to early May 2026 | Full U.S. Senate confirmation vote requiring a simple majority |

| May 15, 2026 | Jerome Powell’s term as Fed Chair ends; target date for Warsh to assume role if confirmed |

| If nomination delayed | Powell may serve as acting chair, or the Vice Chair may preside until confirmation is completed |

While the mechanics of the process rarely move markets, the messaging does. Investors will be listening closely for how the next Fed Chair frames the trade‑offs between inflation and employment and how strongly the institution’s independence is defended, an important sub-context that has been a key focus for markets as President Trump has argued for lower interest rates.

What the Next Fed Chair Inherits

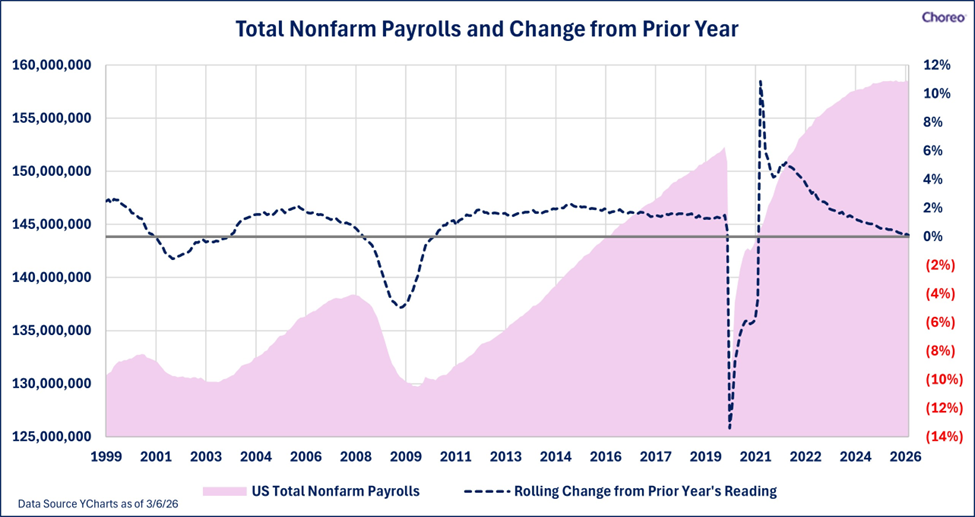

Whoever leads the Fed next will face a challenging, although not unprecedented, environment. Inflation remains above target, growth is steady but not accelerating, and labor markets are normalizing rather than weakening materially, at least thus far. Employment trends can change relatively quickly, similar to what occurred during COVID. Generally, however, the trends move over longer time periods. The chart below shows the total number of employed persons in the U.S. over the last few decades.

What Investors are Watching

As March and April unfold, a handful of developments will be particularly important:

- Status of the Middle East conflict, particularly as it relates to oil prices

- Inflation data for confirmation that progress continues, outside of oil

- Labor market reports

- Shifts in interest‑rate expectations

- Political rhetoric around the upcoming Warsh confirmation

Each of these inputs will help clarify whether the economy is cooling just enough — or not enough — to change the Fed’s calculus.

Conclusion

Periods of policy uncertainty and leadership transition can feel uncomfortable, but they are a normal part of market cycles. Historical data indicates that markets have shown adaptability, and long‑term outcomes are influenced by various factors, including earnings growth, valuations, and diversification, though past performance is not indicative of future results.

As always, our focus remains on maintaining disciplined, diversified portfolios aligned with long‑term objectives. Headlines may change, but the principles of sound investing do not. Please reach out to your Choreo advisor with any questions.

Disclosures

The performance numbers displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Past performance does not indicate future results and investors may experience a loss. The indices discussed are unmanaged and do not incur management fees, transaction costs or other expenses associated with investable products. It is not possible to directly invest in an index.

Opinions are expressed as of the date indicated, are subject to change and are based on sources considered reasonable by Choreo.