“There are two main drivers of asset class returns: growth and inflation.”

~ Ray Dalio, Bridgewater Associates

- Interest rates remain volatile as investors recalibrate the “higher for longer” narrative against incoming data that alternates between cooling and re-accelerating inflation and job growth.

- Energy has re-entered the inflation conversation: the key question is whether higher prices are a short-term shock or the start of broader, stickier pressures.

- Equities continue to take their cues from earnings durability and guidance, with macro variables influencing valuation more than profit expectations.

- Markets are trading on expectations: forward-looking economic measures often move before the official data does.

Late May often feels like a pause: graduation and prom season are under way, summer travel plans are taking shape, and even markets, much like people, seem to catch their breath before the next phase of the year. This seasonal transition offers a natural moment to step back and ask a familiar market question: what’s really driving interest rates (and the market) right now?

It’s tempting to look for a single “first domino” — a hot inflation print, a spike in oil prices, or a Federal Reserve (the “Fed”) headline — but markets rarely move in an orderly sequence. More often, interest rate changes are influenced by multiple narratives: shifting expectations for economic growth, changing confidence in inflation’s path, uncertainty in the labor market, and investors constantly reassessing what those forces mean for policy and risk assets. Much like the chicken-or-the-egg dilemma, the age-old question remains: Is the economic data driving interest rates, or are interest rates driving the data?

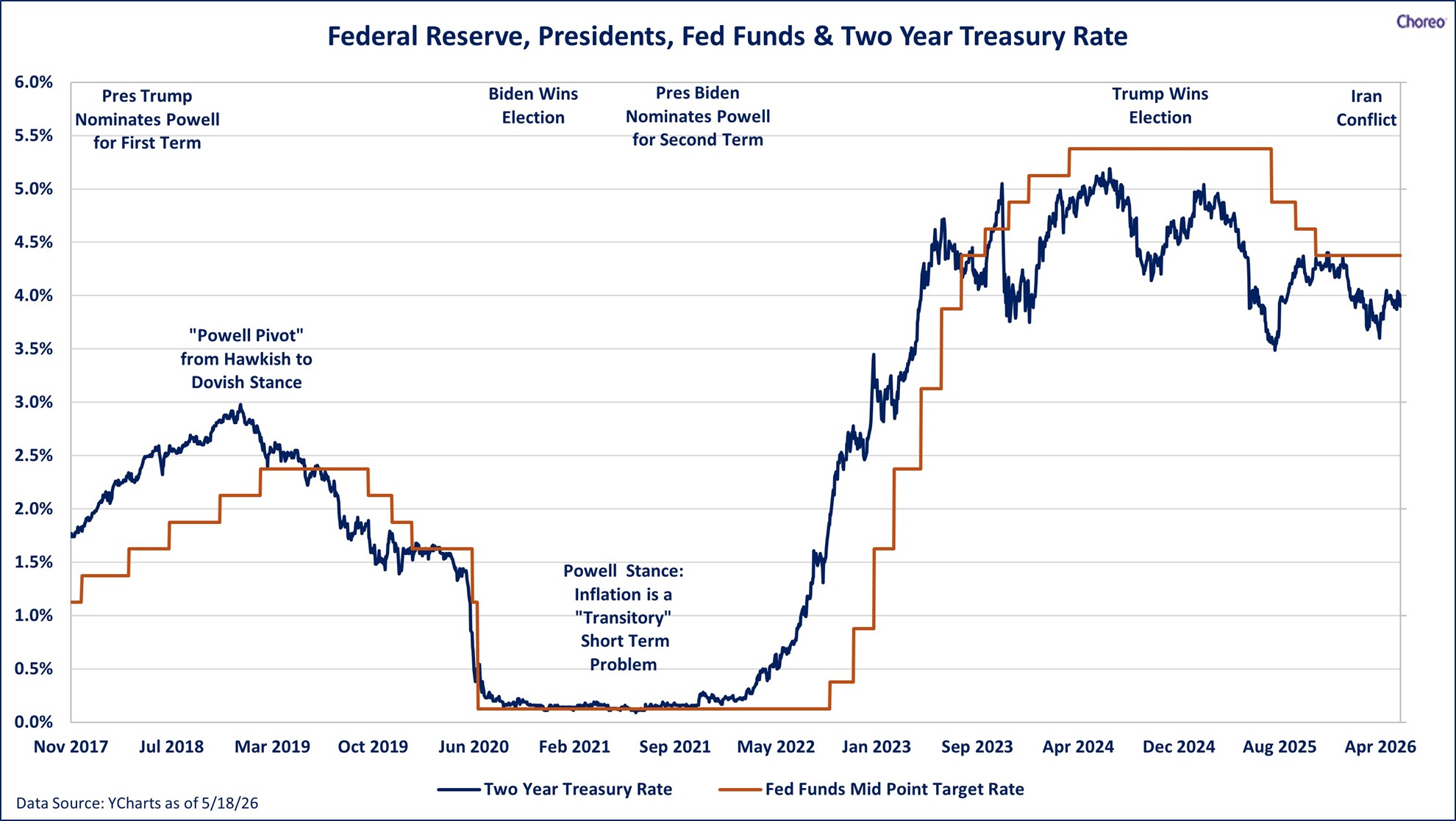

The likely answer is a bit of both, which is where the Fed often chimes in with policy foreshadowing, signaling potential intentions before formal policy decisions are made. Circumstances such as the COVID pandemic clearly drove rates lower to provide a stimulative effect (lower-cost borrowing makes goods and services potentially more in demand), while the increase in rates following the inflationary run several years after was designed to slow the economy by making borrowing more expensive. The graph below shows the interest rate path over the last several presidencies, along with major Fed policy trends.

What Is Really Driving Interest Rates?

Investors often debate whether higher interest rates are being driven by inflation, whether inflation itself is fueled by rising energy and commodity prices, or whether expectations about central bank actions are the true starting point. In practice, rates usually reflect several forces at once, and the primary “driver” can change depending on where we are in the economic cycle and which part of the yield curve we’re looking at.

A helpful framework is to think of longer-term interest rates as a blend of (1) expected real growth, (2) expected inflation, and (3) a “term premium” — the extra compensation investors demand to hold longer-maturity bonds when uncertainty is elevated. Any one of these factors can dominate in the short run, which is why markets may see yields rise even as some inflation measures cool, or fall even when the economic data appears firm.

Inflation: Cause, Effect, or Signal?

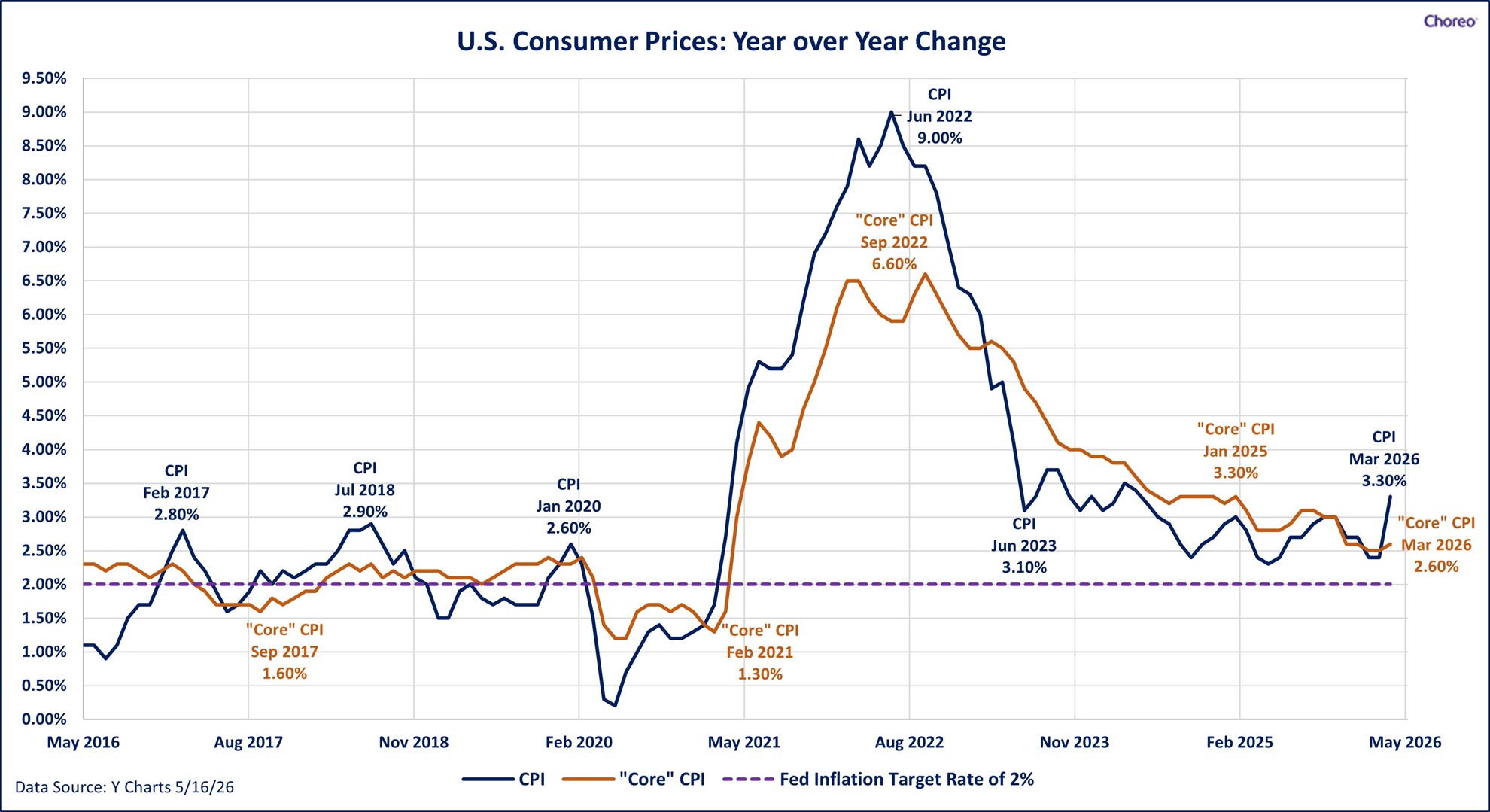

Inflation can be a signal of demand strength, a symptom of supply constraints, or a lagging result of earlier policy decisions. It also comes in layers: headline inflation (measured by the Consumer Price Index “CPI”) captures volatile categories like energy and food, while core CPI measures attempt to isolate the more persistent trend that tends to matter most for long-run policy.

Energy is especially tricky because it acts as both a consumer expense(what households pay at the pump) and a business input cost (what businesses pay to produce and transport goods). A short-lived jump can lift inflation readings without changing the underlying trajectory; a sustained move, however, can seep into broader pricing behavior and expectations — the channel markets watch most closely. The chart below compares core and headline inflation, which can differ based on various components that are more market-driven, such as oil and gas prices.

Sub-Plot: The Energy Factor

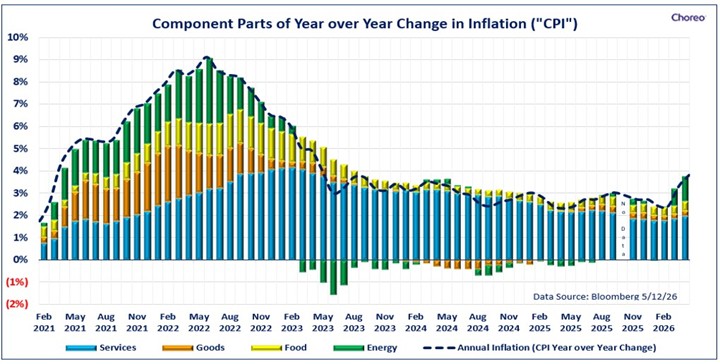

The graph below shows the recent rise in CPI due to oil prices (in green). Oil prices are subject to fluctuations that at times may be driven by headlines and expectations of potential supply shocks. Oil demand fluctuations tend to be modest; however, when supply-side disruptions occur (i.e., war, capacity destruction, etc.), prices tend to spike, as seen during recent tensions in Iran.

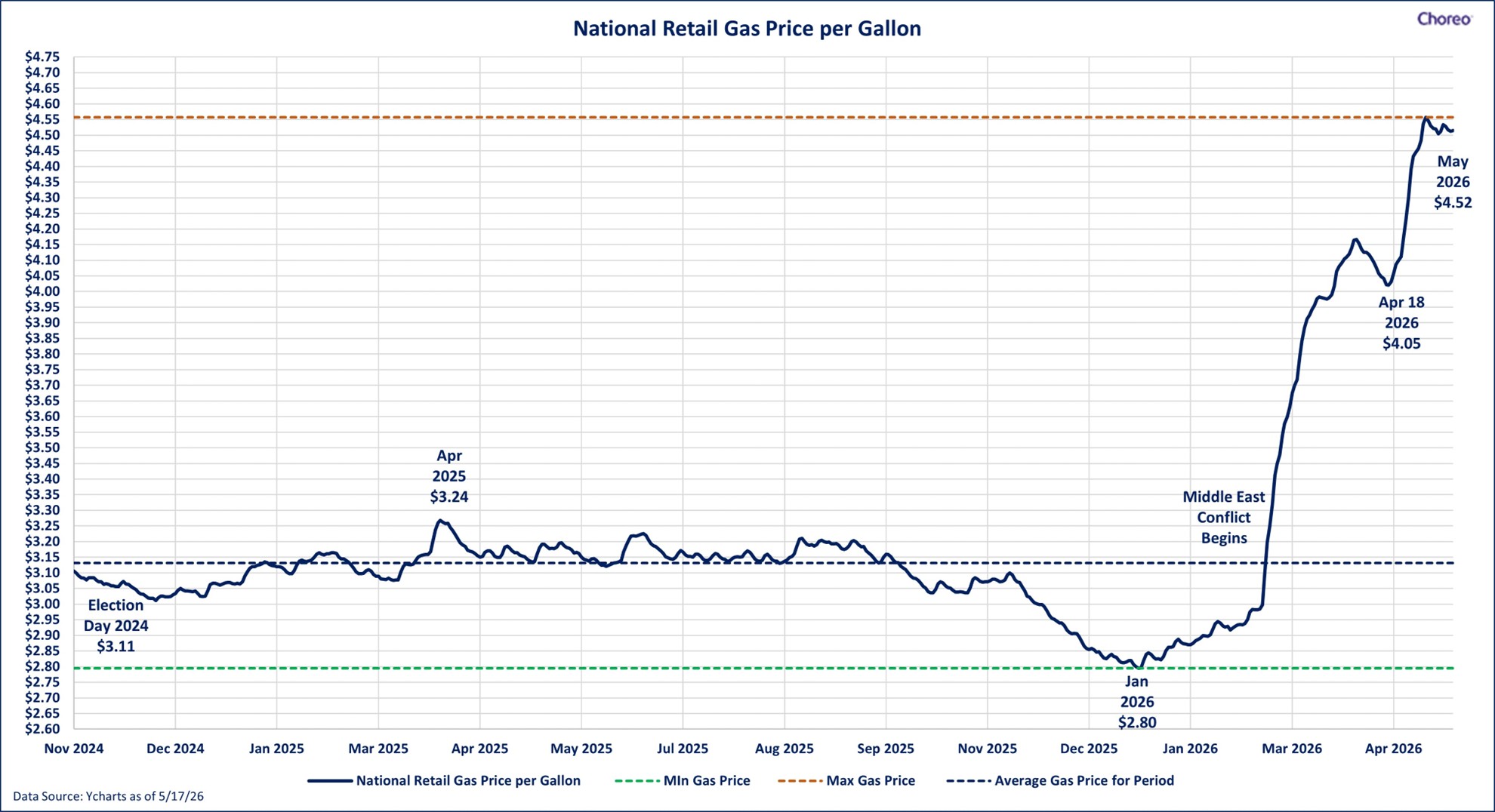

High prices can directly drive consumer behavior as consumers divert precious resources to essential needs. Discretionary spending can become challenged. The average price at the pump has risen precipitously in 2026 as shown in the graph below, potentially limiting further consumer spending, particularly if the high gas prices remain near current levels (or even go higher).

The Federal Reserve’s Role

Central banks react to inflation, labor markets, and financial conditions, but they do so with a lag, since policy decisions are inherently based on backward-looking data. The Fed often tries to identify emerging trends and persistent themes to get ahead of the data, noting that many data sets lag. That’s why the market’s focus is less on the last CPI report and more on the Fed’s reaction function: what combination of inflation progress, employment softening, or financial stress would be enough to prompt a change in policy stance?

Tools like Fed communication, the Summary of Economic Projections, and fed funds futures become “translation devices” between today’s data and tomorrow’s policy. When expectations shift, the front end of the curve (shorter maturities) often responds first and most sharply — sometimes well ahead of any actual policy rate move.

Interest Rates as an Outcome

Rather than being the initial trigger, interest rates often summarize the market’s best estimate of growth, inflation, and risk. When growth is steady and inflation is trending in the right direction, moderately higher rates can co-exist with healthy equity returns — especially if rising yields reflect improving real activity rather than runaway prices.

The challenge is timing and magnitude. Higher rates become more restrictive when they tighten financial conditions enough to slow hiring, curb credit creation, or pressure interest-sensitive areas like housing and small-business financing. In that environment, markets tend to care less about the level of yields and more about what those yields imply for future growth. In other words, rates can dictate economic conditions in the future in a self-fulfilling manner, particularly if the interest rate moves are large on a relative basis.

Equity Markets and the Chain Reaction

Equity markets typically work through rates in two ways: fundamentals (earnings and cash flows) and valuation (the discount rate investors apply). When rate volatility rises, valuation multiples often do the adjusting first — even if earnings remain intact — which can make index performance feel choppy despite solid underlying business results. This year it is easy to blame the volatility experienced in March on earnings growth concerns due to the war. This is likely a portion of the rationale for heightened volatility. However, a larger issue may be the interest rate moves that were based on inflationary fears tied to energy prices rising (which could also slow growth ultimately).

Companies with strong balance sheets, consistent margins, and clear pricing power may hold up better when the cost of capital is uncertain, while more rate-sensitive areas can rebound sharply when markets begin to price easier policy. Over time, though, earnings quality and growth tend to be the anchor.

Why This Matters for Long-Term Investors

Markets rarely move in straight lines or simple cause-and-effect patterns, and interest rates are one of the best examples of that complexity. Trying to “solve” the market in real time often leads investors to overreact to the latest narrative — inflation one week, growth the next, geopolitics and policy expectations the week after.

A more durable approach is to stay diversified across asset classes and factors, to size interest-rate exposure intentionally (especially within fixed income), and rebalance when volatility creates meaningful dispersion. The goal isn’t to predict the next 25 basis point move — it’s to keep the portfolio aligned with time horizon, liquidity needs, and risk tolerance through multiple regimes.

Closing Perspective

As late spring turns into summer, markets — like seasons — continue to evolve. Rather than trying to pinpoint what came first, investors are often better served by focusing on what they can control: maintaining diversification, staying disciplined through volatility, and keeping long-term objectives at the center of every decision. As always, please reach out to your Choreo advisor with any questions or comments.

Important Disclosures

Opinions are as of the date referenced and are based on sources considered reasonable by Choreo. Opinions are subject to change based on market or economic conditions. There is no guarantee that any of these expectations will become actual results.

The performance numbers displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Past performance does not indicate future performance. The indices discussed are unmanaged and do not incur management fees, transaction costs or other expenses associated with investable products. It is not possible to directly invest in an index.

This document contains general information, may be based on authorities that are subject to change, and is not a substitute for professional advice or services. This document does not constitute audit, tax, consulting, business, financial, investment, insurance, legal or other professional advice, and you should consult a qualified professional advisor before taking any action based on the information herein. Information has been obtained from a variety of sources believed to be reliable though not independently verified. Choreo, LLC, its affiliates and related entities are not responsible for any loss resulting from or relating to reliance on this document by any person. Internal Revenue Service rules require us to inform you that this communication may be deemed a solicitation to provide tax services. This communication is being sent to individuals who have subscribed to receive it or who we believe would have an interest in the topics discussed. Past performance does not indicate future performance. The sole purpose of this document is to inform, and it is not intended to be an offer or solicitation to purchase or sell any security, or investment or service. Investments mentioned in this document may not be suitable for investors. Before making any investment, each investor should carefully consider the risks associated with the investment and make a determination based on the investor’s own particular circumstances, that the investment is consistent with the investor’s investment objectives.

All registered trademarks are intellectual property of Choreo, LLC. © 2026 Choreo, LLC. All Rights Reserved.